Gold hasn’t been trading like a safe haven asset since the war with Iran began.

That’s not what a safe haven asset is supposed to do and - of course - the interesting question is why this is happening.

My sense is that the popularity of the “debasement trade” permanently broadened gold’s investor base, so this pro-cyclicality may be a new normal.

There’s one that predates the debasement trade by a couple of years and is about the decoupling of gold prices from real rates.

I’m a fan of the debasement trade and think gold will go a lot higher in coming years.

Thank you for subscribing to my posts. If you’re not yet a paying subscriber, please consider becoming one. That’ll allow you to DM me with questions and comments. I plan to move my posts behind a paywall in coming months. Subscribing now locks you in at a low rate. Thank you so much for your support and feedback!

Yesterday’s post was motivated by a recent ECB report that’s created the impression gold is replacing the Dollar as central banks’ favored reserve asset. That’s not what’s going on. Last year’s big run-up in prices mechanically pushed up the value of central bank gold holdings, making it look like they were adding gold to their reserves, when in fact this was really just valuation gains showing up on central bank balance sheets. There’s been no buying frenzy among central banks and no sign Western sanctions on Russia made gold more sought after.

If anything, the shoe is on the other foot. Gold hasn’t been trading like a safe haven asset since the war with Iran began. Whenever risk aversion spikes, gold falls these days, while it rallies whenever there’s rumors of a peace deal. That’s not what a safe haven asset is supposed to do and - of course - the interesting question is why this is happening. Today’s post is a follow-up to yesterday with a specific focus on how gold has been trading recently and whether its new behavior is permanent.

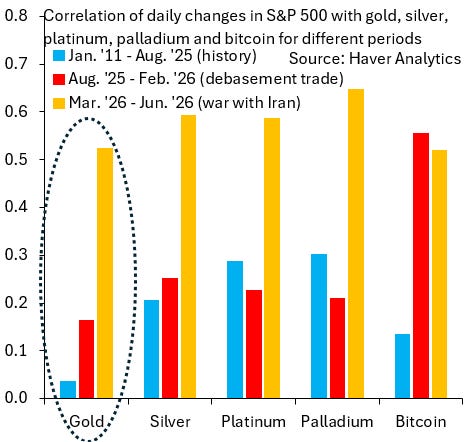

The chart above is one I first published a few months ago and tracks the correlation of gold, other precious metals and bitcoin with the S&P 500. I’m correlating daily returns of each asset, so this is very much a high-frequency focus to see whether gold acts as a hedge for when the S&P 500 - my proxy for risk assets - tumbles. The blue bars are the correlation of daily returns in a long window from Jan. ‘11 to Aug. ‘25, which is before the debasement trade got going. The red bars are the same thing for Aug. ‘25 to Feb. ‘26, which captures the peak of the debasement trade, while the orange bars are the period since we’ve been at war. Gold has historically had a correlation near zero with the S&P 500, but that correlation started to rise last year and is now on par with other - more cyclical - precious metals and bitcoin (which I find shocking).

The interesting thing - of course - is why this correlation switch has happened and whether it’s permanent. My sense is that the huge size of the precious metals run-up in 2025 drew in lots of retail investors who are more skittish than the previous buyer base. My initial reaction - when I noticed this shift - was that it is temporary and that it’ll fade as skittish buyers get flushed out of gold as it sells off. But I’m less sure of that now. My sense is that the popularity of the “debasement trade” permanently broadened gold’s investor base, so this pro-cyclicality may be a new normal.

The correlation shift I discuss above isn’t the only structural break that’s been going on for gold. There’s one that predates the debasement trade by a couple of years and is about the decoupling of gold prices from real rates. The chart above shows this. The blue line is the real 10-year Treasury yield, while the black line is the gold price. The real yield is the opportunity cost of holding gold, since it pays no interest. The fact that the real yield has risen substantially in recent years without pulling gold prices lower is another - even more extreme - structural break. Many link this particular break to sanctions on Russia after its invasion of Ukraine, but there’s no sign that central banks stepped up their gold buying after 2022. In my opinion, this is just another illustration of how retail demand for gold has seen a big surge.

I’m a fan of the debasement trade and think gold will go a lot higher in coming years. After all, fiscal policy is going from bad to worse pretty much everywhere and public debt is only going higher. But I think we also need to accept that the popularity of the debasement trade is making gold more of a cyclical asset than in the past. That’s not the same as saying it’s stopped being an inflation hedge. It still is, but it’s now a high-beta inflation hedge.