Oil prices have fallen back to where they were before the war.

As oil prices spiked in the first weeks of the war, markets switched from pricing cuts for the Fed to hikes.

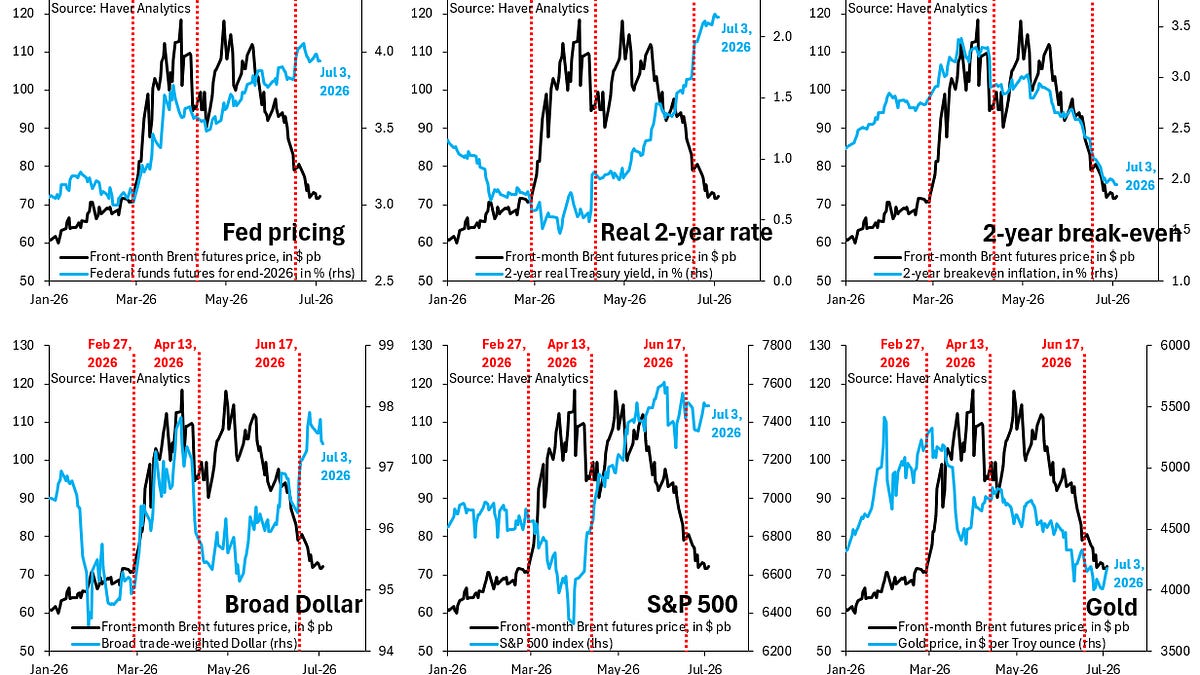

It shows oil prices peaking near $120 towards the end of March and again towards the end of April.

Even though oil prices are back to pre-war levels, markets price more hikes than they have at any point in the past three months.

17 FOMC meeting by several weeks, so this is foremost about the peace deal and falling oil prices.

Thank you for subscribing to my posts. If you’re not yet a paying subscriber, please consider becoming one. That’ll allow you to DM me with questions and comments. I plan to move my posts behind a paywall in coming months. Subscribing now locks you in at a low rate. Thank you so much for your support and feedback!

Oil prices have fallen back to where they were before the war. That in and of itself is remarkable - we’ve blown right through the $80-90 range I’d anticipated as a holding point for at least a few weeks - and stems from the incredibly rapid normalization of oil tanker traffic through the Strait of Hormuz. Factoring in Saudi and UAE pipelines, supply of oil out of the Persian Gulf is almost back to where it was before the war, so it’s fair to say this supply shock is close to over.

You’d think that - with the rapid return of oil prices to pre-war levels - other markets would return to the status quo ex ante as well, but that’s not at all where we’ve ended up. In today’s post, I look systematically across markets to see what’s different. As oil prices spiked in the first weeks of the war, markets switched from pricing cuts for the Fed to hikes. You’d think that would now unwind with falling oil prices, but it hasn’t. Markets have stuck with pricing hikes, which implicitly assumes a hawkish shift in the Fed’s reaction function and means that the post-war equilibrium - as it stands now - consists of a strong Dollar, high real interest rates and deflation.

In my opinion, all this is wrong. Markets are foisting a hawkish narrative on the Fed when there’s little reason for that. Indeed, Warsh second public appearance as Chair this past week sounded dovish and there was never much to substantiate the market’s fixation on a hawkish Fed shift in the first place. After all, the hawkish shift in the dots may be an attempt by some on the FOMC to box Warsh into hikes and get him in trouble with the White House. If that’s true, it won’t work. Falling oil prices will pull inflation down in coming months. The hawkish Fed narrative won’t survive that. This means markets are mis-priced, so I’ll now focus on where this mispricing is greatest.

The format of each of the six charts above is the same. The black line is the front-month Brent futures price, i.e. this line transitions from the May future back in March to the September future currently. It shows oil prices peaking near $120 towards the end of March and again towards the end of April. The three vertical red lines denote the last day before the start of the war (Feb. 27), the imposition of the US blockade on Iran (Apr. 13) and the first FOMC meeting with Warsh as Chair (Jun. 17). The top left chart compares the oil price to what federal funds futures price for the Fed’s policy rate by the end of 2026. This is the blue line on the right axis. Even though oil prices are back to pre-war levels, markets price more hikes than they have at any point in the past three months. The top middle chart shows how this shift in market pricing for the Fed has dragged up the real 2-year Treasury yield, while the top right chart shows that 2-year break-even inflation has fallen alongside oil prices. There’s some who say break-even inflation is falling only because Warsh was hawkish on Jun. 17. That’s not right. The fall in break-even inflation predates the Jun. 17 FOMC meeting by several weeks, so this is foremost about the peace deal and falling oil prices.

The bottom row of charts looks at what this means for markets. The Dollar is up, as the bottom left chart shows, no surprise given the hawkish Fed shift that’s priced. The S&P 500 is up too, which is more of a surprise, but I think that’s due to AI excitement. The bottom right chart show how the hawkish Fed shift has weighed on gold.

Bottom line for me is that markets are wrong to price hikes from the Fed. If I’m right about this, the market implications are immediate. Hikes will get priced out, the real interest rate will fall and break-even inflation will rise. The Dollar will fall and gold will finally start rising again. The S&P 500 should also get a lift. In my opinion, mis-pricing is greatest for the Dollar - where positioning is now very crowded - as well as the very front end of the yield curve. All this should gather steam after the next CPI print on July 14, which should show falling oil prices pulling down inflation.